On November 19, President-Elect Donald Trump announced that Howard Lutnick, CEO of Cantor Fitzgerald and co-chair of his transition team, would be his nominee for Commerce Secretary. Lutnick’s company Cantor Fitzgerald and its subsidiaries are multinational in scope, promote the implementation of the United Nations’ Sustainable Development Goals (which have major implications for debt politics and economic activity), and are even directly partnered with foreign state-owned firms that recently came under scrutiny following the release of the contents of the laptop of the current (and recently pardoned) First Son, Hunter Biden.

Lutnick had previously been angling for a job as incoming Treasury Secretary, an unsurprising ambition given Cantor Fitzgerald’s outsized role in the U.S. Treasury market (i.e. the U.S. government debt market) and its relationship to dollar stablecoins, which are rapidly becoming one of the main purchasers of U.S. debt. It is unknown currently why Lutnick was passed over for Treasury, despite endorsement for the position from Elon Musk and RFK Jr., and appointed to Commerce instead. However, Trump’s previous Commerce Secretary, Wilbur Ross, was widely believed to have been given the role to repay a past favor of major significance. In Ross’s case, it was his assistance in rescuing Trump from bankruptcy in the early 1990s. At the time, Ross worked for Rothschild Inc., and when clarifying why the European banking dynasty had bailed out the future President, Ross stated “the Trump name is still very much an asset.” Shortly before, Rothschild Inc. had been bankrolling the entry of Robert Maxwell, intelligence asset for Israel and arguably the Soviet Union, into the American economy, with a specific focus on New York City.

During and following the campaign, Lutnick has been a major supporter of Trump’s prospective plan to implement an extensive tariff regime in lieu of income tax. If confirmed, Lutnick will also oversee the approval of the export of sensitive technology of national security interest abroad, negotiate free trade agreements, and oversee the patents office, among other roles. While mainstream reports on his appointment have noted his “hawkish” trade stance with China and his connections to the cryptocurrency agency, much has been left out about Lutnick, his current business entanglements and historical connections to intelligence networks that have sought to undermine the Commerce Department specifically to facilitate the transfer of sensitive U.S. military technology to ostensible adversary states, like China.

Satellogic: Observation is Preservation

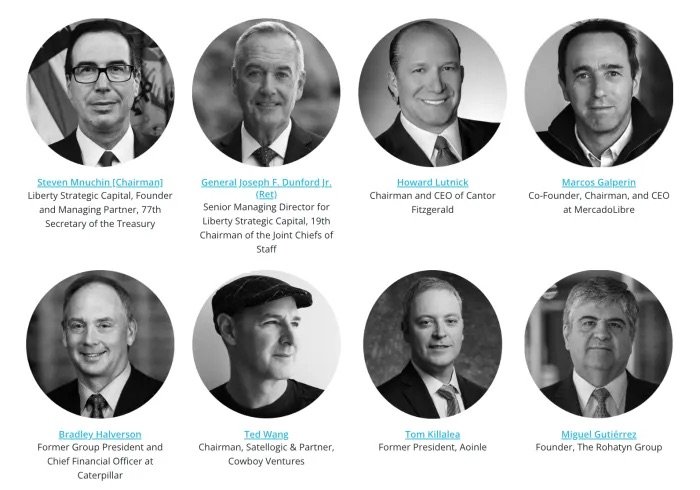

In exploring these issues, it is useful to look at one company now closely tied to Lutnick – Satellogic. Lutnick sits on Satellogic’s board, as does former Treasury Secretary from the previous Trump administration Steve Mnuchin and former head of the Joint Chiefs of Staff under Trump, General Joe Dunford. Mnuchin and Dunford invested heavily in Satellogic through the private equity they now work for, Liberty Strategic Capital. Mnuchin has led that firm since its founding. Liberty Strategic Capital’s first investment was in a controversial Israeli intelligence-linked cybersecurity firm called Cybereason. Cybereason’s co-founder and CEO Lior Div has described Cybereason as a continuation of his work in Israeli intelligence outfit Unit 8200, where Div worked on offensive cyber attacks targeting foreign nations. The firm became controversial in the lead-up to the 2020 election for simulating, along with U.S. security agencies like DHS, the necessary threshold of cyberattacks that would induce the cancellation of a U.S. presidential election and the imposition of martial law. Lutnick himself has significant ties to Israel and is a well-known billionaire mega-donor to Israeli and Zionist causes (discussed in detail later in this article).

Debt From Above: The Carbon Credit Coup

Latin America is quietly being forced into a carbon market scheme through regional contractual obligations – enforced by the satellites of a US intelligence-linked firm – which seeks to create an inter-continental “smart grid,” erode national and local sovereignty, and link carbon-based life to the debt-based monetary system via a Bitcoin sidechain.

Satellogic, for its part, employs a former Israeli intelligence officer, Aviv Cohen, as its head of “special projects.” Cohen previously co-founded Fraud Sciences Corp. with Unit 8200 alum Saar Wilf, which was later sold to PayPal and now forms the “back-bone” of its anti-fraud algorithm. Prior to that, Cohen worked for Core Security Technologies, the firm previously co-founded by Satellogic’s co-founders that contracted for numerous U.S. intelligence and military agencies. Since we reported on Cohen’s ties to Satellogic earlier this year in April, Satellogic has made Aviv Cohen’s biography on the company website private.

In an interview with Bloomberg in January 2022, Lutnick and Mnuchin expressed the reasoning behind their venture into Satellogic via Liberty Strategic and CF Acquisition Group V, a subsidiary of Lutnick’s Cantor Fitzgerald. “We felt that space and the satellites in particular is really the next coming gigantic market for data,” explained Lutnick. “I mean, to have images of the whole Earth – data on the whole Earth – the amount of decisions that will unlock, and the ability and the economics of how that will unlock, was extraordinary.” Lutnick furthered that their proprietary lens technology allows customers of Satellogic to “count the containers on the ships,” “count the cars,” “count the trees,” or “count the number of [panels] working and what’s not working in a solar farm,” which “unlocks a vast, vast sea of opportunity in marketplaces.”

In the same interview, Mnuchin expressed similar excitement about the opportunities downstream of such detailed Earth observational technology, but with a telling insight on how said data, when paired with artificial intelligence, can advance the interests of the national security state and increase government-led markets. “We’re very focused on investments where not only can we bring capital but we can bring our expertise. And we’re particularly focused on the technology area, national security, and other forms where we can add a lot of value,” Mnuchin articulated. “So what we liked about this is great technology, very scalable, very affordable, and the combination of having a lot of data with a lot of AI really will enable both very big government markets, and more importantly, very big commercial markets.”

Lutnick’s Cantor Fitzgerald, one of 24 primary dealers of the New York Federal Reserve, is no stranger to participating in the financing of the data broker industry, having given $100 million in equity financing to Near Intelligence Holdings’ effort to go public in May 2022. Near was founded by Idealab’s Bill Gross, the first institutional investor in PayPal, and currently boasts being “the world’s largest source of intelligence on people, places and products.” An October 2023 report by the Wall Street Journal revealed that Near had “provided data to the U.S. military via a maze of obscure marketing companies, cutouts, and conduits to defense contractors.”

While Near business model operates in the shadows, feeding off data scraped from clever advertising mechanisms and unread user agreements behind mobile applications, Satellogic is directly attacking the billions of potential revenue from “creat[ing] all new types of markets” downstream of “scalable, affordable imagery,” according to Mnuchin. Lutnick, in the same conversation with Bloomberg, boasted that Satellogic can “take a video from space of more than a minute of an airport and tell you the brand of plane that is taking off,” in his argument that “this kind of data is such a big market.” Lutnick added that “imagery from satellites” is “one of the world’s great marketplaces.” Echoing that same line of thinking, the former Treasury Secretary stated that he views Satellogic “as more of a data company than necessarily just a space company,” which can leverage “vast amounts of data” in order to “really analyze climate issues, energy supply, food security,” and “supply chains.”

In regards to climate issues, Lutnick claims that Satellogic’s technology will “finally end the concept of climate change” by “literally remap[ing] the Earth every day.” The death of the specific concept of climate change alluded to by Lutnick seemingly refers to the popularized “left wing” modeling of the climate emergency, versus the likely incoming “right wing” carbon market, as articulated in previous reporting from Unlimited Hangout. An unspoken wrinkle in the pricing of carbon, as proposed independently by Lutnick and fellow-Trump advisor Elon Musk, is the dollar denomination and thus the implications on the sale of United States’ Treasuries. In an idea to be explored later in this article, a carbon market denominated in dollars may not solve the “climate crisis,” but it just might help solve the ever-looming debt crisis.

This position has already been taken by Lutnick’s Tether, as the purchasing of government bonds by the stablecoin issuer continually increases in volume and remains poised to become systemically important, as covered in previous reporting by Unlimited Hangout. While Lutnick’s immense connection to the Treasury market – whether through Cantor Fitzgerald itself or its custodial relationship and investment in Tether – led many to believe he was in position to become Treasury Secretary, Trump picked him for Commerce Secretary, and thus placed him in a management position over many public sector entities directly related to his private-sector activities such as Satellogic.

The “very strong, patentable technology” built by Satellogic, as explained by Mnuchin, takes on a new meaning with the appointment of Lutnick to the Department of Commerce (DOC), due to the DOC management of the U.S. Patent and Trademark Office (USPTO). This is far from the only conflict of interest within Lutnick’s venture into the public sector, as the DOC manages many bureaus directly impacted by the proliferation of a U.S.-based, private-sector Earth observation company such as Satellogic. Some of the dozen bureaus under the DOC relevant to Satellogic – not to mention Lutnick’s position within the digital asset space via Cantor’s relationship with Tether – include the Bureau of Economic Analysis (BEA), the Bureau of Industry and Security (BIS), the International Trade Administration (ITA), the National Technical Information Service (NTIS), and the National Telecommunications and Information Administration (NTIA), not to mention the aforementioned NOAA, and USPTO.

Interestingly, the DOC also established the U.S. AI Safety Institute dedicated to upholding the asks within the October 2023 Biden-Harris executive order on “the Safe, Secure, and Trustworthy Development and Use of Artificial Intelligence.” In October 2024, the Biden-Harris administration issued the first ever national security memorandum on AI, empowering the DOC to “harness power of AI for U.S. national security.” Previous U.S. government-sponsored commissions, such as the National Security Commission on AI, had concluded that it was necessary to ensure U.S. military and economic hegemony by forcing American consumers off of “legacy systems” and onto AI-powered alternatives, lest American AI companies lag behind their Chinese counterparts, particularly in the fields of e-commerce and finance. They also made the case for increased, AI-powered mass surveillance – such as that facilitated by Satellogic – as a means of advancing this cause.

In August 2021, the Lutnick-linked Tether, via its subsidiary Northern Data, purchased over 223,000 GPUs (graphical processing units) used in AI computing from the cryptocurrency firm block.one, which was founded by Tether co-founder Brock Pierce. A month later, the stablecoin issuer spent nearly half a billion dollars purchasing Bitcoin miners from block.one in a deal facilitated by Christian Angermeyer, a long-time friend of Palantir’s Peter Thiel. Palantir, which has long-standing and very close ties to the CIA, is a Satellogic partner and Palantir co-founder Joe Lonsdale donated heavily to Trump (as did Palantir itself) while Thiel has extremely close ties with the incoming Vice President J.D. Vance.

Since Lutnick’s Cantor Fitzgerald helped take Satellogic public via SPAC, Satellogic – founded in Argentina and previously based in Uruguay – has now redomiciled in the United States in an effort to obtain lucrative government contracts. The company’s move to Delaware was prompted by Satellogic’s poor financials after going public. However, government contracts have been slow to appear for the firm, with Satellogic securing its first government contract with NASA just this past September. However, a Lutnick-run Commerce Department could alter Satellogic’s chances in securing future contracts. This conflict of interest between Lutnick’s private sector dealings with his newfound government appointment was noted by Politico in October 2024, which claimed that Lutnick was “improperly mixing his business interested with his duties standing up a potential administration.” According to the report, Lutnick took meetings on Capitol Hill under the guise of transition team matters, then “allegedly us[ed] the opportunity to talk about matters impacting his investment firm, Cantor Fitzgerald,” which also included “high-stakes regulatory matters involving its cryptocurrency business.”

The board of Satellogic as of early 2024 (Bradley Halverson was recently replaced); Source – Satellogic

This conflict of interest is notable in part because some of the bureaus Lutnick will oversee as Commerce Secretary, such as the NOAA, are targets of Satellogic’s contracting ambitions. For instance, Satellogic markets itself as able to measure carbon emissions from space and has promoted its recent NASA contract as part of the government effort to target climate change. NOAA and other agencies housed under the Commerce Department collect climate data for the U.S. government. As will be noted again shortly, Lutnick was an early pioneer of electronic carbon emissions trading and his company is a major advocate for the implementation of the UN’S SDGs, part of an over-arching UN-supported plan that includes using space satellites to measure carbon emissions.

Last year, the NOAA granted Satellogic a remote sensing license, helping secure “Satellogic’s strategy to capitalize on high-value opportunities in the U.S.,” specifically as it relates to U.S. government contracts. The license grants Satellogic NOAA oversight and the ability to secure contracts with U.S. defense and intelligence agencies, a major goal of the company per Satellogic president Matt Tirman.

Satellogic was co-founded in 2010 by CEO Emiliano Kargieman and CTO Gerardo Richarte after spending “some time” at the NASA Ames Campus in Mountain View, CA. Both Kargieman and Richarte previously worked for Core Security Technologies, which was co-founded by Kargieman and boasted national security state clients such as Homeland Security, NSA, NASA, Lockheed Martin, and DARPA. In 1998, Core Security was recognized as an “Endeavor Entrepreneur” by the Endeavor Foundation, whereas Satellogic’s eventual seed round raise was funded by Endeavor’s Santiago Pinto Escalier, in addition to Ariel Arrieta and NXTP Ventures, and the Kargieman-advised Starlight Ventures. Kargieman later founded Aconcagua Ventures in a joint venture with Craig Cogut’s Pegasus Capital, and served as a Member of the Special Projects Group at the World Bank. Pegasus Capital became the main funder of Satellogic-partner CC35, a group seeking to impose a fraudulent carbon market on much of Latin America, as covered in previous reporting from Unlimited Hangout.

Another Core Security Technologies employee that migrated to Satellogic with Kargieman and Richarte is Aviv Cohen, the aforementioned ex-Israeli intelligence officer who is now Satellogic’s head of “special projects.” Chinese tech giant Tencent, which owns a significant stake in Elon Musk’s Tesla, also invested in Satellogic’s Series A, as did Endeavor Catalyst, which is run by LinkedIn/PayPal’s Reid Hoffman, and Valor Capital, whose partners include figures tied to U.S. military and intelligence activities in Latin America, a former CEO of PayPal, as well as CBDC development on the continent. Valor is also advised by Brian Brooks. Brooks was a former employee at OneWest Bank alongside Mnuchin, and was made Acting Comptroller of the Currency in May 2020 via Mnuchin’s designation, where he introduced “regulatory initiatives that provided banks with the green light to offer cryptocurrency custody services and stablecoin payment systems.”

In February 2022, Palantir – a private sector intelligence firm led by PayPal-founder Peter Thiel and created with CIA funds to replace a controversial DARPA mass surveillance and data-mining program – committed to a five year strategic partnership with Satellogic. Satellogic’s partnership with Palantir enables its “government and commercial customers”, which include the CIA and J.P. Morgan, access to Satellogic’s Aleph platform APIs to feed raw satellite imagery to Palantir’s MetaConstellation and Edge AI. This partnership builds on a previous collaboration between Satellogic and Palantir to “field unique AI capabilities to the orbital edge,” including “live upgrades to the satellite’s onboard AI” that enables “an ultra-low-latency maritime use-case.” Palantir and Satellogic customers, which include the Pentagon’s Space Systems Command, Space Force, SpaceX, the government of India, and others, will soon have access to the Edge AI platform running on Satellogic satellites “to offer customers tailored AI insights.” This is expected to increase Satellogic’s business of “data products, streamline pipeline management, and further scale customer delivery required for weekly and daily world remaps.” Some of their customers, like the government/military of Ukraine, have been applying both Palantir and Satellogic “insights” directly to the battlefield for over two years. This underscores that Satellogic’s technology is clearly intended for use in both civilian and military settings.

Epstein Entanglements

In 2022, Satellogic signed a far-reaching agreement with Elon Musk’s SpaceX, itself a major U.S. military and intelligence contractor. SpaceX remains Satellogic’s “preferred launch provider” for launching its satellites into near-Earth orbit. During the campaign and since the election, Lutnick and Musk have collaborated extensively, with Musk even endorsing Lutnick for his preferred nomination as Trump’s incoming Treasury Secretary.

Notably, Musk’s SpaceX was allegedly infiltrated by Lutnick’s former next-door neighbor, intelligence asset, pedophile and sexual blackmailer Jeffrey Epstein. Epstein reportedly introduced a member of his “entourage” to Musk’s brother Kimbal, then on the board of SpaceX. That young woman, who had previously “dated” Epstein and lived at the 301 66th St East apartment complex now known to have housed women Epstein trafficked, then dated Kimbal Musk from 2011 to 2012. As a consequence, the relationship with Kimbal “brought Epstein into contact with the Musk family and its businesses.” This allegedly culminated in Epstein touring SpaceX facilities in 2012, a claim a SpaceX attorney very belatedly denied after the incident was first reported by Business Insider. Kimbal Musk is also on the board of another of his brother’s companies – Tesla – and, prior to his 2019 arrest, Epstein confirmed claims from sources that he was privately advising Tesla in 2018 to journalist James Stewart. After Epstein was infamous, Musk denied the claims. Per Stewart, Epstein was apparently part of the attempted deal to take Tesla private with Saudi money in 2018. Epstein was also a very close advisor at that time to the then and current de facto leaderMuhammad bin Salman.Since then, an Epstein associate turned venture capitalist, Nicole Junkermann, has become a significant investor in SpaceX.

From Left to Right: Kimbal Musk, Tosca Musk, Maye Musk and Elon Musk at the SpaceX-NASA launch in May 2020; Source – Kimbal Musk’s Instagram

In addition, Elon Musk himself was subpoenaed as part of the now-shuttered USVI lawsuit against the bank JP Morgan for its role in facilitating Epstein’s crimes and is known to have socialized with Epstein and Ghislaine Maxwell on several occasions prior to Epstein’s 2019 arrest and death later that same year. In one such meeting, brokered by LinkedIn co-founder Reid Hoffman, Musk was reported to have introduced Epstein to Mark Zuckerberg of Facebook/Meta. Musk also attended the Edge Foundation’s “billionaire dinners,” which courted top figures in Silicon Valley and operated as a de facto front for an Epstein-run influence operation for several years, coinciding with the genesis of the “billionaire dinners.”Furthermore, Richard Sorkin, the CEO of Elon and Kimbal Musk’s first company Zip2, joined an Israeli intelligence-linked tech company headed by Ghislaine Maxwell’s sister Isabel Maxwell shortly after the sale of Zip2 to Compaq in 1999.

In addition, Musk shares some business links to Epstein associates. For instance, a major supplier to Tesla, LS Power (via its subsidiary EVgo), and its affiliated hedge fundLuminus Management are closely linked to Jonathan Barrett, who was a managing director of LS Power and has led Luminus Management since 2011. Barrett also held several other senior roles at LS Power between 2003 and 2008. Barrett is a former protégé of Jeffrey Epstein’s who started his career working at Epstein’s firm J. Epstein & Co. and also became the CFO and Vice President of Ossa Properties, the real estate firm run by Epstein’s brother Mark and co-founded by Barrett’s brother Anthony. Barrett listed his legal address for many years as being 301 66 St East in Manhattan, an apartment complex that is majority owned by Ossa that housed many of the women actively being trafficked by Jeffrey Epstein and which was frequented by Epstein’s associates, including several who stayed overnight, like former Israeli Prime Minister Ehud Barak.

LS Power, where Barrett was a top executive, has been investigated “for fraudulent conveyance of assets” in several bankruptcy cases. In addition, LS Power’s founder, Mike Segal – whose son Paul is now the firm’s CEO, did business with the Bufalino crime family. Luminus Management was also the largest shareholder in Valaris, which sold $650 million in oil rigs to Musk’s SpaceX in 2020. In addition, another firm closely linked to Luminus – Luminus Capital Management and the Luminus Capital Partners Master Fund – counts Alex Erskine as a director. Erskine was previously a director for the Jeffrey Epstein-chaired financial vehicle Liquid Funding, which was partially owned by Bear Stearns before its collapse during the 2008 financial crisis.

As recently noted, Howard Lutnick was the long-time next-door neighbor of Epstein’s now infamous New York townhouse at 9 E. 71st St. Lesser known perhaps, is Epstein’s long history with that property and that connection of the entity that ultimately sold the home to Lutnick. Lutnick’s address, 11 E. 71st St., was first purchased by a Leslie Wexner-controlled entity called SAM Conversion Corp in 1988, a year before the Nine East 71st Street Corp. (of which Epstein was president) bought the neighboring home. In 1992, SAM Conversion Corp. – with Epstein now its Vice President – sold the 11 E 71st St property to the 11 East 71st Street Trust – where Epstein was a trustee – for “ten dollars and other valuable consideration paid by the party of the second part,” according to Crain’s New York. During this time, Leslie Wexner “refurbished” the property at 9 E. 71st St. for tens of millions of dollars, which included adding an unusual “security system” reportedly later used to record videos, allegedly for the purposes of blackmail, once Epstein inhabited the residence. It is unknown if similar “refurbishments” were made to the neighboring house later bought by Lutnick that was also under Epstein/Wexner control at the same time.

In 1996, with Epstein already inhabiting 9 E. 71st St. for at least a year, the neighboring home at 11 E. 71st St. was sold to Comet Trust for “ten dollars and other valuable consideration.” Some reports have suggested the price paid for the home was around $6.2 million. The trustee of Comet involved in the sale was Guido Goldman, the son of famous Zionist Nahum Goldman, a very close friend of Henry Kissinger and founder of the German Marshall Fund, which later spawned the controversial Alliance for Securing Democracy. Goldman was also the apparent liaison between the Council on Foreign Relations (CFR) and the CIA. At the time the sale was made to Goldman and the Comet Trust, Epstein was also part of the CFR and, according to a 2001 report in the UK’s Evening Standard, told people that he had once worked for the CIA.

Epstein’s former New York home, neighboring Lutnick’s, at 9 E. 71st St.; Source – Kuekue Dunia

The Comet Trust was one of three trusts established “for the benefit of descendants of the late Minda de Gunzberg,” who was born Minda Bronfman and was the sister to Charles and Edgar Bronfman. Their father, Sam Bronfman, built the family liquor empire in large part to his ties to organized crime elements during the American Prohibition era. Charles Bronfman co-founded the “Mega Group” with Leslie Wexner in 1991, which spawned Birthright Israel, an organization that counts the Lutnicks as among their top donors. In addition, Edgar Bronfman was arguably the main player in the insider trading scandal that allegedly resulted in Epstein leaving Bear Stearns in 1981. Edgar’s son, Edgar Jr., also appears in Epstein’s black book of contacts and Edgar’s daughters, Sara and Clare, were central figures in the NXIVM sex cult scandal. The Comet Trust later sold the home to Howard Lutnick, again for “10 dollars and other valuable consideration” and Lutnick took out a $4 million mortgage on the property the same day the sale was made. Lutnick has never publicly commented on his property’s history or any information regarding his relationship with his former next-door neighbor.

Notably, Edgar Bronfman Jr. heavily funds and chairs the start-up accelerator network, Endeavor, which backs Satellogic, among other companies. Another major backer of Endeavor is Pierre Omidyar, a major donor to Clinton and Obama with a long history of collaborating with U.S. intelligence. (Lutnick himself was a major donor to Clinton’s 2016 presidential campaign and has long backed a variety of Democrats before deciding to back Trump relatively recently.)

In addition, alongside Lutnick on Satellogic’s board is Marcos Galperin, Argentina’s richest man, who is considered Endeavor’s earliest success story and who maintains close ties to the organization. Endeavor targets emerging market start-ups specifically and is also very closely connected to a close associate of Jeffrey Epstein’s, LinkedIn co-founder Reid Hoffman. Another major figure in the Endeavor network is Eduardo Elzstain, an Argentine oligarch who – like many other Argentines connected to Endeavor – has cultivated close ties to current president of Argentina Javier Milei. Elzstain, a long-time associate of George Soros, hosts the Argentine equivalent of Bilderberg – the annual, closed-to-the-public Llao Llao Forum which is frequented by members of Endeavor Argentina. Elzstain is also on the board of the WJC – whose long-time president was Edgar Bronfman Sr. Elzstain also boasts close ties to the apocalyptic-messianic Chabad Lubavitch movement, which has significant ties to Donald Trump, Trump’s son-in-law Jared Kushner, and also to Howard Lutnick.

Lutnick and the Search for Dollar Debt Sinks

In addition to being backed by Endeavor, Satellogic is now also backed by Tether, which boasts important ties to Lutnick. Cantor, which is “majority-owned by its CEO Lutnick,” was recently revealed to be a 5% owner of Tether after a $600 million investment, according to reporting from The Wall Street Journal. The assumed largest shareholder of Tether, co-founder Giancarlo Devasini, reportedly told the paper that “Lutnick will use his political clout to try to defuse threats facing Tether.”

While already pegged for Commerce Secretary and verbally committed to stepping down as CEO at Cantor upon Senate confirmation, Lutnick is currently working closely with Trump by “vetting candidates for other top government jobs that could involve supervising Tether.” While naturally the regulation on stablecoin issuers would have profound implications for Tether and its minority-owner Cantor, the importance of this blossoming industry as a net-buyer of government bonds in an era of high inflation (and $36 trillion in already-issued debt) pegs Tether and its ilk as systemically important to the United States government’s survival.

In order for an incoming Trump administration to successfully meet the demands of their congressional budget, while also servicing our compounding trillions in debt already owed, the Treasury needs to find a willing buyer for that newly issued debt. In the past 18 months, a new high volume net buyer of this debt has appeared in the form of stablecoin issuers, such as Tether or Circle, which have purchased over $150 billion of U.S. debt in the form of securities issued by the Treasury in order to “back” the issuance of their dollar-pegged tokens with a dollar-denominated asset. For some perspective, China and Japan, historically the U.S.’ largest creditors, hold just under and just over $1 trillion, respectively, in these same debt instruments. Despite only existing for a decade, and only surpassing a $10 billion market cap in 2020 – the same year Trump’s OCC passed a bulletin allowing U.S. banks to hold stablecoins – Tether is already earmarked for over 10% the Treasuries held by either of the U.S.’ largest nation-state creditors. As previously mentioned, Tether’s impressive stash of Treasuries are custodied by Lutnick’s Cantor.

Using stablecoins as a method to mitigate the U.S. debt problem has been circulating among Republicans for some time, including former Speaker of the House Paul Ryan, who articulated this exact sentiment in a recent op-ed with The Wall Street Journal titled “Crypto Could Stave Off a U.S. Debt Crisis.” Ryan claims that “stablecoins backed by dollars provide demand for U.S. public debt” and thus “a way to keep up with China.” He speculated that “the [debt] crisis is likely to start with a failed Treasury auction,” which in turn leads to “an ugly surgery on the budget.” The former Speaker predicted that “the dollar will suffer a major confidence shock” and as a result asks, “What can be done?” His answer is to “start by taking stablecoins seriously.” Tether’s CEO Paolo Ardoino echoed this sentiment, referring to Tether as “the best friend of the U.S. government,” due to “hold[ing] more U.S. Treasury securities than Germany, much more than any other competitor or any other financial institution in the world.” Tether also notably is partnered with U.S. agencies like the FBI and Secret Service.

Dollar-backed stablecoins are arriving as “an important net purchaser of U.S. government debt,” Ryan notes, with stablecoin issuers now the 18th largest holder of U.S. Debt. Ryan goes on to say that “if fiat-backed dollar stablecoin issuers were a country,” that nation “would sit just outside the top 10 in countries holding Treasurys,” still less than Hong Kong but “larger than Saudi Arabia,” the U.S.’ former partner in the petrodollar system. Ardoino articulated that Tether is “happy to decentralize the ownership of the U.S. debt, making the U.S. much more resilient.”

Satellogic, and thus Tether and Cantor, are also involved in the development of carbon markets and predatory climate finance endeavors. Cantor was a pioneer of electronic carbon emissions trading and continues to promote climate finance as well as implementation of the UN’s Sustainable Development Goals (SDGs). Satellogic positions itself as able to measure carbon emissions from space, a policy supported in the UN document “Our Common Agenda” and has begun to attempt to do this via GREEN+, as covered in previous reporting by Unlimited Hangout.

NOAA, which granted Satellogic a license and which Lutnick will oversee, collects climate data for the government and the Commerce Department in general would play a major role in establishing any form of “carbon pricing,” whether a carbon market, as Satellogic is helping to build, or a carbon tax, a policy long supported by prominent Trump backers like Elon Musk. Naturally, the promotion of a carbon tax –tellingly proposed by one of the world’s richest men who also happens to own the largest EV company in the world – would simply further the class divide that currently exists in the United States, with the rich having no problems upgrading to emission-free vehicles nor meeting the expenses brought on by such a tax system. The actual enforcement, and thus the successful creation, of such a proposal requires exactly the type of data provided by an Earth observation company – a field in which Satellogic stands somewhat alone.

Carbon pricing is simply not possible without government-vetted, accurate measurements of carbon molecule density, and thus the market for reliable data service providers has quietly been dominated by Satellogic. As the debt instruments of the private sector evolve alongside the proliferation of blockchain technology, the data that makes these smart contracts execute to eventually settle no longer goes to a human arbitrator, but rather a consciousness-free protocol that reduces a pair of potential outcomes to a single output. This oracle and settlement protocol is seemingly poised to be the blockchain, at least that is the argument made in this piece, and exemplified by many of the affiliates and partners of Satellogic, including Lutnick. These novel green finance instruments can be upheld and paid out by blockchains and smart contracts, including the Bitcoin-sidechain Rootstock, which was listed on documents as being another partner of GREEN+ alongside Satellogic and CC35.

Additionally, such as in the case of Satellogic partner O.N.E. Amazon, entities can create entirely new blockchain protocols to issue and uphold settlement of tokenized “real world assets,” known as RWAs. O.N.E. Amazon is chaired by Peter Knez, who oversaw the creation of ETFs (exchange traded funds) while heading Barclay’s iShares division. iShares is now owned by BlackRock after being purchased in the aftermath of the 2008 financial crisis, and features the fastest growing ETF in history, the iShares IBIT Bitcoin ETF.

“Sustainably” Surveilling and Tokenizing Nature: The Case of O.N.E. Amazon

The architect of BlackRock’s ETFs has teamed up with a group of companies tied to US intelligence and US government debt trading to tokenize the Amazon rainforest and borgify it with a large-scale sensor network in order to create a new form of “digital gold.”

O.N.E. Amazon aims to create “sustainable impact for the environment and investors by using next-generation technology to bring innovation to conservation.” The “innovation” O.N.E. Amazon offers is related to its issuance of a capped-supply of “regulated O.N.E. Amazon Digital Asset Securit[ies].” Per Knez, “each security will represent the perceived value of one hectare of biome in the Amazon rainforest, backed by a 30-year preservation agreement over that land,” capped at 750 million, “corresponding to the hectarage of the rainforest.” In other words, each security issued represents one hectare of the Amazon. O.N.E Amazon asserts that “investors will benefit from the potential capital appreciation of the security” in large part due to “the finite size” of the rainforest it is tokenizing.

Knez co-authored a paper with Mysten Labs – founded by former Facebook/Meta employees who helped develop their stablecoin project, Libra/Diem, as covered in previous reporting by Unlimited Hangout – titled “Preserving Nature’s Ledger: Blockchains in Biodiversity Conservation,” which promotes a framework that focuses on “tokenization strategies for biodiversity species and for IoT [internet of things] solutions, such as sensors, drones, and satellites to monitor and record data related to species and ecosystems.” Satellogic isn’t the only concerning firm partnered with O.N.E. Amazon, for instance, Aecom, – the successor to the CIA-linked Ashland Oil – currently contracts extensively with USAID, which is widely believed to be a CIA front organization. Interestingly, Knez’ co-founder, Rodrigo Veloso, played a significant role in the efforts to take Trump Media & Technology Group (TMTG) public, the parent company of the Trump-centric social network Truth Social.

With the carbon credit market and tokenized RWAs presenting themselves as the preferred debt instruments of the modern era, Lutnick’s Satellogic finds itself ready to act as a crucial pillar of the encroaching new financial system, assuming the U.S. can get other nations to participate in these new technology spheres. This is the role that the Department of Commerce has previously and controversially played, and thus worth investigating the recent history of the DOC as Lutnick prepares to commandeer it.

The Commerce Department and the Legacy of “Chinagate”

Though Lutnick’s aforementioned ties to the Epstein-Wexner-Bronfman network are circumstantial, Lutnick’s ties to the government of Israel (which had a significant relationship with Epstein) and Zionist causes are numerous. Indeed, Lutnick has said that his main reason for deciding to work with the Trump campaign was because of Trump’s extreme pro-Israel stance, with Trump having personally told Lutnick’s wife Alison that “I will be the best President for Israel.”

In that past year, Lutnick’s Cantor Fitzgerald Relief Fund, has donated heavily to support Israel’s genocidal war in the Gaza Strip in addition to $7 million the fund gave “to support those impacted by the way in Israel.” A portion of this went to the Israeli volunteer-based emergency services organization, United Hatzalah, which is itself a member of the World Economic Forum and whose founder Eli Beer, an Israeli real estate mogul, has been a WEF Young Global Leader and award recipient from Klaus Schwab’s Schwab Foundation for Social Entrepreneurship. Lutnick and his wife chaired United Hatzalah’s United Hatzalah annual fundraising gala earlier this year. United Hatzalah became infamous in some circles last year for fabricating claims of Hamas brutality on October 7th, including claims of a baby burnt in an oven, that the organization later admitted were untrue.

Lutnick’s appointment to be Commerce Secretary is significant in light of the fact of his ties to Israel, Zionist organizations and his circumstantial ties to the Epstein nework, as Israel – and Epstein specifically – were part of a major, largely forgotten scandal of the Clinton era that culminated with the apparent murder of Clinton’s Commerce Secretary Ron Brown and many employees of the Commerce’s International Trade Administration (ITA) office. Commerce and ITA had been targeted by figures tied to both the Chinese government and Israel with the goal of transferring sensitive U.S. military technology, mainly satellites, to China in exchange for the covert arms smuggling of banned Chinese weapons into urban centers in the U.S. West Coast. At the time, those urban centers were also being targeted with a CIA-manufactured crack cocaine epidemic, as reported by the late Gary Webb. The smuggling of arms into these areas was obviously meant to be aggravate a multi-pronged effort by what was essentially the Iran-Contra network (of which Bill Clinton had been part) to decimate minority communities in West Coast urban centers, with the apparent goal of facilitating the growth of the private prison industry and the prison labor pool.

As detailed in the book One Nation Under Blackmail, the Commerce Department – and the ITA specifically – deals with the export of non-agricultural U.S. products abroad, and was apparently the main target of what is now remembered as a “campaign finance scandal” often referred to as “Chinagate.” However, the scandal – though intimately involving Chinese government-owned firms – is significantly larger than China in scope and should be seen as a continuation of the CIA-Israeli intelligence nexus responsible for illegal operations that harmed American national security, such as those that formed the bulk of the Iran-Contra scandal under the Reagan and Bush administrations. Bill Clinton had been intimately involved with the Iran-Contra nexus while he was governor of Arkansas, which was partially facilitated by his long-time connection to his political benefactor Jackson Stephens, who was also tied to Iran-Contra. Ultimately, this is where the group responsible for the genesis of Chinagate can be found.

Meet Mark Middleton with Ed Berger

In this episode, Whitney is joined by researcher extraordinaire Ed Berger to unravel the mystery behind the recently deceased Mark Middleton, the man who met with Epstein well over ten times at the Clinton White House. Originally published 09/15/22.Podcast available on Rokfin, Soundcloud, Apple Podcasts and Unlimited Hangout. Podcast available now on all Podcast apps,…

Stephens and his business partners, the Riady family, were largely responsible for the hiring of main Chinagate figures like Johnny Huang to the Commerce Department’s ITA. Shortly before Chinagate began, the Riadys became business partners of the Chinese government. Other central figures in Chinagate, like Mark Middleton and C. Joseph Giroir, were connected to and later employed by the Riady family directly as the scandal unfolded. Middleton, notably, was the main person whom Jeffrey Epstein would visit at the Clinton White House. Most of those visits were made in the lead-up to the 1996 presidential election, the election around which the “campaign finance scandal” aspect of Chinagate took place.

The campaign finance aspect of Chinagate ultimately served to grant non-American citizens, like the Riadys and their allies, unprecedented access mainly to Ron Brown, then head of Commerce. The Riadys and their associates used several “strawmen” to mask illegal campaign contributions to Clinton’s re-election campaign. There were also American businessman who sought special access to Brown, like Bernard Schwartz of Loral, who had been the biggest donor to the DNC for the 1996 election and used his access to Brown to secure meetings with major Chinese politicians and businessmen in charge of state-owned enterprises. A separate probe into Loral was opened as Chinagate began to be investigated, as Loral-produced satellites were discovered in the hands of Chinese military-linked firms and because of apparent evidence that Loral had facilitated “an unauthorized transfer of missile technology” to China. Schwartz had previously used his influence to lobby the Clinton administration to move approvals for satellite exports abroad from the State Department, to Brown’s Commerce Department.

Bill Clinton (center) and Ron Brown (right) participate in a meeting on April 3, 1993, Source: US Presidential History

Meanwhile, other figures in Chinagate successfully pushed Clinton to ban Chinese weapons imports (the U.S. was then their largest market for guns) in order to secure Congressional approval of “most favored nation” trade status for China. However, figures brought into close contact with Clinton by the Chinagate nexus, like China’s “top weapons dealer” Wang Jun, were later involved in efforts to illegally smuggle very large amounts of those banned weapons into the U.S. Those smuggling efforts were later partially foiled by the FBI in what is now referred to as Operation Dragon Fire. However, the top operatives – including those linked to Wang Jun – that were involved in the smuggling effort were tipped off and managed to escape the U.S., with only their underlings ultimately taking the blame.

Yet, there is also the possibility that the Iran-Contra era airline that had previously been involved in arms smuggling and drug trafficking in the Reagan/Bush era may have played a role in keeping it going. An American billionaire with close ties to both China and Israel, Leslie Wexner, and his close associate Jeffrey Epstein were involved with the re-location of that CIA-linked airline, Southern Air Transport, from Miami to Ohio and shifted its main routes from between North, Central and South America to between Ohio and Hong Kong. Ohio officials at the time suspected that the change in route and Wexner’s acquisition of the airline was linked to organized crime and, just years prior, Ohio law enforcement had produced documentation (which was later heavily censored) linking Wexner directly to organized crime interests. Meanwhile, Epstein cultivated close ties with key figures in Chinagate simultaneously, particularly with Mark Middleton – who was later killed in a murder made to look like a suicide after Epstein’s extensive visits with him at the Clinton White House were made public.

Middleton was not the only figure in Chinagate to suffer a grisly fate. Just as “Chinagate” was beginning to come to light, Ron Brown and much of the top brass at the ITA were “asked unexpectedly to travel to Croatia.” The “unexpected” travel offer was made shortly after Brown agreed to a plea deal where he would have testified in probes that would have exposed a significant part of the “Chinagate” nexus if he had been able to testify. The Croatia trip, however, ended in tragedy when the plane carrying Brown and top Commerce personnel crashed, killing everyone on board. President Clinton publicly said the crash was due to “a peculiar mix of circumstances” and, three days after the crash, the head of navigation at the Croatian airport allegedly “responsible” for the crash was found dead, shot in the chest. His death was quickly ruled a “suicide.” At the crash site, strange anomalies were found by the U.S. military investigators who responded to the scene, who identified an apparent gunshot wound in Brown’s skull that, obviously, would not have caused by the crash itself.

A US military helicopter hovers near the crash site of the flight that had carried Ron Brown and other top Commerce officials in Croatia; Source – The Dubrovnik Times

Ultimately, proximity to Epstein and the state of Israel is complicated when one considers the long-running and documented history of Israel passing sensitive American security technology shared with “our greatest ally,” a phenomenon that preceded and continued after the “Chinagate” scandal. Thus, Howard Lutnick’s ties not only to Israel and his circumstantial yet proximal relationship to Epstein should be scrutinized as should Lutnick’s business ties to China. For instance, the BGC Group, which Lutnick controls, has a joint venture with the Chinese state-owned China Credit Trust. China Credit Trust is the largest shareholder in Harvest Fund Management, which created BHR Partners alongside the Hunter Biden-linked firm Rosemont Seneca and the Thornton Group, headed by James Bulger, nephew of the infamous mobster James “Whitey” Bulger.

Notably, another figure in Trump’s sphere (though not poised to serve a formal or informal role in his next administration) – Blackwater founder Erik Prince – is closely financially connected to one of the main Chinese firms that had been involved in Chinagate, CITIC, which is the largest shareholder in Prince’s Frontier Services Group.

Lutnick, The Dollar and Financial Control

The reason behind exploring the role the Department of Commerce has played in the Chinagate and Iran-Contra scandals is not to falsely associate the incoming Lutnick-led DOC with historical corruption – seeing as how Lutnick has plenty of his own controversial connections and conflicts of interest, as detailed above – but rather to demonstrate the decades-long technology transfer as a necessity for imperial economic hegemony.

While the United States has been history’s most recent empire of choice for imposing a unilateral economic paradigm on much of the world in the post-World War II era, the groups that have long dominated the American establishment – or more appropriately the Anglo-American establishment – have been working for over a century to create “a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole.” Per historian Caroll Quigley, this system would be controlled in “feudalistic fashion” by principally bankers, who hammer out secret agreements at frequent private meetings and conferences.

Samuel Pisar, a prominent lawyer for major U.S.-based corporations, stepfather to current Secretary of State Anthony Blinken, and one of the closest friends and confidants of Robert Maxwell, openly told Congress in 1971 that this global system of financial control in private hands had already arrived. Pisar spoke of this system as the rise of the “transideological corporation,” where the firms of the “capitalist” West were merging and/ or forging significant agreements or joint ventures with the state-owned businesses of the “communist” East. The result, per Pisar, was that “all conventional tools of national policy” had become “anachronistic” and that nation states were no longer “dependable economic entit[ies].” Pisar, who declined to condemn this phenomenon, noted that the two main vehicles driving the rise of this global system of financial control in private (or semi-private) hands are the rise of the multinational corporation, technology transfer and the dominance of the US dollar outside of American domestic markets, e.g. the Eurodollar market. Now, with much of this global financial control system well-established and entrenched, the world can be more easily on-boarded onto a single, hegemonic currency controlled by entities that ultimately answer to the now hegemonic “transideological corporation.”

The successful proliferation of a new financial system across the globe with digital dollars native to the internet is innately reliant on broadband internet, cellular network providers, readily-available smartphones powered by economical microprocessors, and wide-spread operational knowledge of every pillar upholding blockchain technology. The technological infrastructure needed to issue digital securities, “decentralize” government debt, tokenize parcels of the rain forest, or to uphold a carbon market, bring about many surveillance concerns that come downstream of the realities of a completely digital economy.

The technology transfer – led in no small part by various iterations of the DOC – has enabled a globalized, internet dollar and thus severely neutered the ability of non-U.S. central banks and governments to retain capital within their border. Interestingly, the infrastructure upholding the national security interests of the United States is dominated by private sector, U.S.-based FinTech stalwarts, including the owners of the fiber optic cables running beneath our oceans and Satellogic’s satellites-as-a-service orbiting our skies. This legal or Constitutional barrier between the public sectors interests and the private sector that builds the technology actualizing said interests allows the data brokers that glean information directly from these technological spigots to package and sell user data to both private and public entities alike. In few industries is this concept more dangerous for the freedom and privacy of global citizens than it is within the purely digital economy perpetuated by Lutnick’s Tether, and the e-carbon market regime made possible by Lutnick’s Satellogic.

Despite the populist momentum present in U.S. political rhetoric since the dominating election night display put on by the incoming Trump administration, the country finds itself in a perilous position. Well, it certainly would be if not for the technology-driven financial revolution waiting in the (West?) wings. With the nation nearly $40 trillion dollars in the hole, and with defense spending now outpaced by simply servicing the interest on said debt, if it wasn’t for the private sector rescue unit – led in no small part by companies affiliated with Lutnick – the incoming Red-branches of American power would be facing a serious crisis. Thankfully, the global technology transfer needed to facilitate the dollarized panopticon has long been completed, and the hegemonic-weakening leaks in the proverbial dyke have been plugged by the likes of Tether and Satellogic, whose few competitive predators – be it fellow American FinTech companies or international intelligence affiliates – now find themselves at the whim of a Department of Commerce and executive branch all-but-ready to play king-maker via regulation and enforcement.

At the end of the day, the government is no different from a corporation, with a budget needing to be serviced alongside personnel and hiring requirements – both of which demand high quantities of high fidelity data. This data will be sequestered, distributed, and parsed via the fiber optic cables, the microprocessors, the blockchains and the satellites the U.S. produces. It is thus certainly fitting then that the next phase of American empire will once again be upheld by private companies and the likes of our new Commerce Secretary Howard Lutnick.

While many Republicans for years have railed against the official narrative around climate change and many of the solutions promoted to mitigate it, climate finance is poised to make a comeback over the next 4 years, despite Republicans taking both the White House and the legislature by a significant margin. This is because many of the most influential names in the incoming Trump administration, as well as the previous one, have become intimately involved in creating carbon markets in recent years, while others have a long-standing track record of pushing carbon taxes and other forms of “carbon pricing.”

Chief among these is Howard Lutnick, the co-chair of Trump’s transition team who has stated that he is tasked with finding the “talent” for the incoming administration. Lutnick is the long-time and current head of Cantor Fitzgerald, which was one of the earliest players in emission trading and has since become a global leader in ESG investing, “sustainable infrastructure” financing and green bonds. For example, Cantor’s sustainable infrastructure fund is expressly committed to “digital transformation, decarbonization and the improvement and modernization of aging infrastructure,” while “a primary focus for the Fund will be to invest in issuers that are helping to address certain United Nations Sustainable Development Goals through their products and services.” In addition, the top constituent of another Cantor infrastructure fund is Invenergy, a renewable energy company that has received a significant amount of subsidies from the Biden’s controversial Inflation Reduction Act and is run by the country’s first “wind billionaire” Michael Polsky.

The Satellogic board

Lutnick also servers on the board of a satellite surveillance company called Satellogic. In addition to Lutnick, former Trump Treasury Secretary Steve Mnuchin chairs its board and also on the board is Joe Dunford, the former head of the Joint Chiefs of Staff of the U.S. military under Trump. Satellogic is an integral part of a consortium attempting to use opaque contractual agreements at the municipal level to impose a massive, blockchain-based carbon market on Latin America. That carbon market, operating under the name GREEN+, is poised to be built on a Bitcoin side-chain and, as previously reported, its carbon credit scheme is deeply inequitable for Latin American communities. For instance, the only money communities could make from the scheme would be only available for GREEN+-approved “sustainable” projects while GREEN+ members would reap the bulk of the profits. The program would also subject communities to Satellogic’s satellite surveillance apparatus (tied to the U.S. government and Israeli intelligence) without their consent.

In addition, GREEN+ is notably tied to figures close to Trump’s allies in the region. For example, a major figure in Nayib Bukele’s political party – San Salvador mayor Mario Durán – is a vice president of one of the main groups orchestrating the GREEN+ scheme while the Endeavor Argentina network, which has very close ties to Argentina’s Javier Milei, is also very closely linked to Satellogic. For instance, Satellogic itself is an Endeavor-backed company while Endeavor’s first billionaire entrepreneur, Marcos Galperín of MercadoLibre, serves on Satellogic’s board. In addition, a major investor in Satellogic, the dollar stablecoin issuer Tether, is also closely connected to Howard Lutnick. Lutnick is a long-time major advocate of Tether and Cantor Fitzgerald custodies the bulk of Tether’s U.S. Treasuries that back up their stablecoin and its peg to the U.S. dollar.

In addition to Lutnick, prominent Trump backer and donor Elon Musk, who has pledged to work with Lutnick to usher in an unprecedented age of government “efficiency,” has invested heavily in carbon removal technology and even created a $100 million prize to spur new carbon removal methods. Musk also previously broke ties with Trump during his previous administration after Trump pulled out of the Paris climate agreement in 2017. He is also a long-time advocate for carbon taxes. Musk previously lobbied the Biden administration on implementing a carbon tax, a policy supported by Biden’s Treasury Secretary Janet Yellen.

Yet, under the Trump administration, the push for a carbon tax was led by Republicans, reflecting the policy’s bipartisan support. That Trump-era proposal, known as the Baker-Shultz plan, called to repeal emissions regulations from the Environmental Protection Agency and a roll-back of some Obama-era climate policies in exchange for replacing them with a carbon tax. The plan was framed as a way to “let the market decide” how to price carbon as opposed to government. Something similar could be deployed by the next Trump administration as a “compromise” that would see the Biden-era climate policies that Trump campaigned against rolled back in exchange for the implementation of some form of “carbon pricing,” like a carbon tax.

The Baker-Schultz plan is named for James Baker and George Schultz, two Republicans who served in the Reagan and Bush Sr. administrations. This is notable as it was during the Bush Sr. administration that emissions trading was first created with government support. The father of emissions trading, first for sulphur dioxide and then again for carbon, is Richard Sandor, a former executive at the scandal-ridden, corrupt Drexel Burnham Lambert (Drexel’s most notorious criminal – Michael Milken – was pardoned by Trump during his previous term). Drexel was a key figure in the financial scandals of the 1980s, including the Savings & Loans crisis which had intimate ties to James Baker and the Bush family as well as the CIA and organized crime.

Sandor is also considered the father of financial derivatives and helped draft the cap and trade component of the Kyoto Protocol. He did so in direct collusion with Maurice Strong, the architect of Agenda 21 – the pre-cursor to the UN Sustainable Development Goals. Strong was also a long-time associate of David Rockefeller, an oil magnate and a notoriously corrupt UN official who later had to flee North America to China due to his involvement to the UN’s oil-for-food scandal. Sandor subsequently was a major influence on Obama-era climate policies, but also has close ties to Trump-era figures, like J. Christopher Giancarlo – who was made chair of the CFTC by Trump in 2017. Giancarlo, a major advocate of turning the U.S. dollar into a programmable, surveillable private sector digital currency, has called Sandor “one of the true visionary developers of new financial products.”

Ultimately, emissions trading itself was originally a Republican policy and has since been promoted in bipartisan fashion for several decades. While Trump did pull the U.S. out of the Paris agreement, the out-sized role of Lutnick and Musk (who cut ties with Trump last time over climate policy) in shaping his next administration’s policies and cabinet picks suggests that Trump has now softened his stance on “market-based” climate solutions. For anyone that has followed Trump’s policy record from his first term, it was quite clear that Trump – like any American politician – is usually willing to give Wall Street what it wants. Some examples of him doing this include giving Larry Fink, the veritable king of ESG, near complete control over U.S. fiscal policy during Covid, resulting in a massive wealth transfer, and Trump also deregulated the banking industry despite campaigning in 2015-2016 on reinstating Glass Steagall and other regulations on the biggest banks. (Other industries whose products have major environmental and public health consequences, such as GMO crops, were also heavily deregulated during the first Trump administration.)

Trump Embraces the “Bitcoin-Dollar”, Stablecoins to Entrench US Financial Hegemony

Trump’s recent speech on bitcoin and crypto embraced policies that will seek to mold bitcoin into an enabler of irresponsible fiscal policy and will employ programmable, surveillable stablecoins to expand and entrench dollar dominance.

Though it’s certainly true that Republicans in the legislature have largely rejected carbon taxes and markets earlier this year, the fact that Trump has surrounded himself with climate finance advocates and the fact that Wall Street needs climate finance to unlock an entire new asset class to fuel their casino (lest it collapse) are strong indicators that some sort of “carbon pricing” is in the works. Even prominent figures in the “MAHA” “unity” movement, like former RFK Jr. VP pick Nicole Shanahan have advocated for using tokenized carbon credits to facilitate U.S. government money printing (i.e. “quantitative easing”) and U.S. debt management. With a U.S. debt crisis in the cards and Howard Lutnick, one of the biggest traders of U.S. government debt, at the helm of choosing Trump’s next cabinet, the likelihood of a carbon market has never been higher, despite the recent Republican victory.

Featured Image: Elon Musk (right) speaks at an October 2024 Trump campaign rally alongside Howard Lutnick (left)

A monetary network’s success is dependent on the size and volume of its active user base.

The former lead of Facebook’s Libra project, David Marcus, is the former President of PayPal. PayPal’s founding mission, and subsequent T-shirt motto, was to create “A New World Currency.”

Marcus built Facebook’s stablecoin project after concluding that Bitcoin lacked the qualities to be a successful medium of exchange.

In order to appear decentralized, Libra formed the Libra Association, but included many very inter-connected businesses and people, as noted elsewhere in The Chain series.

Government regulators, fearing Facebook’s immense active user base, quickly called the Libra team to testify before Congress, and eventually pressed the project to fold before launching.

Libra had previously stated in their S-1 filings that regulatory pressure and uncertainty could lead the project to never launch. Other evidence suggests the entire goal of Libra was to perfect the public-private partnership for the future implementation of the U.S. government’s preferred digital currency project.

Jared Kushner sent an email to Steve Mnuchin in May 2019 regarding a Sam Altman post on stablecoins titled “US Digital Currency.”

Mnuchin’s Treasury then held a March 2020 meeting after inviting many figures mentioned in The Chain series, including Wences Casares and Peter Thiel.

Libra announced partnerships with Fireblocks, Silvergate Bank, and Paxos in order to expedite their stablecoin project, but none materialized.

After being shutdown by regulators, Libra sold off its assets to Silvergate Bank in January 2022.

Silvergate facilitated Bitcoin-collateralized loans with MicroStrategy and Marathon Digital, and were partially owned by Block.One, BlackRock, State Street and Citadel Securites.

Silvergate Bank, whose SEN product serviced a substantial amount of firms mentioned in The Chain series, was then liquidated by regulators in March 2023.

Silicon Valley Bank (SVB), which failed two days after Silvergate, banked a significant amount of the companies and venture capital in the cryptocurrency industry.

The day before the SVB collapse, Peter Thiel’s Founders Fund pulled out funds, and advised clients to do the same, triggering deposit flight.

10 customers alone had $13 billion in deposits at SVB, and $42 billion left the bank in 6 hours. In other words, SVB collapsed due to an acute liquidity crisis that was spawned by very few people.

The Trump administration’s deregulation of the banking industry in 2018 loosened capital and reporting requirements, leading to many of the issues seen in the banking crisis in 2023.

Circle’s USDC stablecoin, which had $3.3 billion of reserves at SVB, would “depeg” to 86 cents during the crisis.

Six months after the banking crisis, and two weeks after the U.S. House Financial Services committee advanced their first stablecoin bill, Paxos and PayPal launched PYUSD.

The Gillibrand-Lummis Stablecoin Bill was directly influenced by the Terra-LUNA collapse, which resembles more of a controlled demolition than an organic collapse. As a result, the bill bans algorithmic alternatives in pursuit of preserving the dual banking system. Both Senator Gillibrand and Senator Lummis have significant donor ties to many of the firms mentioned in The Chain series.

Large lobbying groups, such as Coin Center and the Digital Chamber of Commerce, were formed to help guide legislation as it relates to stablecoins and digital assets. Both of these lobbying groups have advisory ties to stablecoin issuers and many firms and people mentioned thus far in The Chain series.

Multiple parties mentioned in this piece, from the Libra team to lobbyists, have echoed the sentiment that USD stablecoins can help retain the U.S. dollar as the world’s reserve currency.

Many of the companies formed after the dissolving of Libra carry on the work of building a new financial system based on stablecoins and public blockchains.

According to national security state members, Bitcoin and stablecoins can provide a “boon for surveillance” in addition to helping grow the economy.

The Bitcoin-Dollar system, as described in The Chain series, is the actualization of PayPal’s founding intention to create a “new world currency”, and it was carefully constructed to appear as an organic phenomenon when it is not.

The initial trio of pieces in The Chain series have focused on the three essential pillars for creating a new digital monetary system. The first, The Chain of Custody, examined the construction of novel custodial infrastructure to enable the secure holding of billions of dollars worth of digital assets after the proliferation of Bitcoin as a new financial class. The second, The Chain of Issuance, investigated the primordial roots of digital payments fortifying data brokers and information bankers within the global surveillance network. It also noted how stablecoin issuers are the modern day analogue to the influence that the major infrastructural titans of the Industrial Age had on the formation of The Federal Reserve in the first half of the 20th century. The third, The Chain of Consensus, focused on the currency speculators and intelligence-connected developers behind the monetary policy and consensus infrastructure of privately-issued money and the blockchain revolution during the infancy of the Deflationary Age brought about by Bitcoin and the subsequent, dollarized iterations of its underlying database technology.

In summary, a new financial system cannot be built without the ability to custody assets, issue new assets, and uphold the settlement and monetary policy of said assets via a governing consensus. Yet, even with the successful formation of this necessary trifecta, the construction of a monetary network is simply fruitless without the acquisition of the last remaining pillar: a network of active users. This concept is well understood by both the private sector companies that have been mentioned throughout this series, in addition to the public sector that currently acts as the enabling environment for the rules and regulations of nation-state monetary systems upheld by central banks across the world. None of these public issuers of money, however, have the global impact of the U.S. Federal Reserve and the U.S. Treasury system, which provides immense privileges that come downstream from their issuance of the notes and reserves backing the world reserve currency, the U.S. dollar. With 66 countries worldwide listing the dollar as an official currency, the vast number of users utilizing these instruments makes the dollar system the largest financial network in the world.

Even within this monopoly, there is a fractured set of settlement networks, such as PayPal, and private banks, such as J.P. Morgan, issuing said dollars in users’ checking accounts. This balkanization presents a unique opportunity for further consolidation and, with that consolidation, the ability to acquire even more users. For example, PayPal acquired millions of global users via their purchases of Venmo and Xoom, while J.P. Morgan assumed the deposits of the failed First Republic Bank after the onset of the regional banking crisis in 2023.

Money itself is but a technology that enables agreeable and predictable outcomes between two bartering parties. This axiom requires money that simultaneously acts as a unit of account, a store of value, and a medium of exchange. While all of these properties can be met by a multitude of currently circulating currencies – and even commodities – their usefulness for settlement across both time and space is determined nearly entirely by the number of users within their respective networks. The dollar system is the most liquid monetary network in the world, and has held this position for nearly a century. Historically, the world’s reserve currency has held its dominant status for roughly this same duration of time. With U.S. debt levels now growing at uncontrollable and exponential rates, the formation of proposed alternatives to the dollar’s monopoly are popping up across the globe. The world economy is a finite pie consisting of finite users, and with the dollar network appearing truly weak for the first time in decades, competitors are posturing for a piece. However, with the global broadband internet dissolving some of the control that nation states have over their own citizens’ monetary choices, the world is actually dollarizing faster than ever.

As the internet age enters its third decade, the stakes for creating the internet of money have never been higher. For now, the proliferation of dollarized blockchains seemingly aims to fortify the dollar’s hold over global finance, not dissolve it. Regardless of the dollar’s domination of denomination, the upstart issuers of these tokenized assets have hemorrhaged away enough users that it now threatens many of the privileges the legacy system once enjoyed, mainly the available profits found by selling their data and leveraging their deposits.

The understanding that social networks are communication platforms, and that money itself is just a ledger upholding the communicative expression between users, led the social media giant Facebook to experiment with adding financial instruments to their vastly popular Messenger app. While Bitcoin and alternatives had been around for nearly a decade before Facebook’s Libra was proposed, this was “the shot heard ’round the world” for central bankers and regulators to sit up straight and take a novel payments system proposed by the world’s largest social network seriously.

Yet, as Facebook soon found out, if you come at the king, you best not miss. Or at least this was the story that was told to the world: The U.S. regulatory system said “No” and that was that. However, this concluding piece to The Chain series, The Chain of Command, postulates that Libra was never intended to actually go to market as designed, but rather was meant to set the stage for clear regulation via legislation that would become the enabling environment for a decades-long attempt at creating a new world currency by the very same parties covered thus far in this series.

Libra, Diem and Facebook’s Stablecoin

Sitting on a Caribbean beach during the winter of 2017, David Marcus was struck with the idea of creating a global digital currency to run on Facebook’s Messenger. Marcus, who had sold his mobile payment provider Zong to PayPal for $240 million in 2011, and who had been introduced to Bitcoin in 2009, was certainly no spring chicken to the rapidly evolving FinTech and digital payments space. Within nine month of Zong’s acquisition by PayPal, Marcus was named PayPal’s president in April 2012. Then, in June 2014, Marcus was recruited by Facebook’s Mark Zuckerberg to run their Messenger app. By the time the idea that would become Libra began to germinate during his 2017 vacation in the Dominican Republic, the social network’s messenger app boasted over 1.3 billion active users.

Prior to his experience with PayPal and Facebook, Marcus had founded GTN Telecom, noted as being the “first to break Switzerland’s telecommunications monopoly” in 1996. GTN Telecom was backed by the UK’s 3i, a venture capital firm founded in 1945 by the Bank of England and “a syndicate of British banks,” and was later sold in 2000 to WorldCom’s World Access just two years before WorldCom would file for Chapter 11 bankruptcy after excessive accounting fraud. Marcus went on to found Echovox, a “mobile monetization company focused on monetizing web and traditional media audiences” via “transaction-enabled mobile services,” shortly after the October 2000 sale of GTN. Zong was later spun off from Echovox. Bertrand Perez and Kurt Hemecker, two executives at Zong, would become part of the founding team at Libra alongside Marcus.

“In late 2009 when I first stumbled upon Bitcoin and read the white paper, I tried to play with it, but it was so cumbersome even for a geek like me. I just couldn’t get it. So I kind of put it aside, brushed it aside, and then came back to it in 2012 when a good friend of mine who’s often referred to as a Patient Zero in Silicon Valley for Bitcoin, [Xapo’s] Wences Casares, basically started telling me more about it and telling me ‘you have to actually spend time and understand this thing.’ And so I did. And then I just couldn’t stop thinking about it. I just couldn’t stop thinking about this idea that you could actually be your own self-sovereign for digital value and you could move it around without any intermediary in between…

Then in 2013 at PayPal, that’s after Zong got acquired by PayPal and I was running it, I remember that Argentina asked us to actually stop the flow of money going out of the country from PayPal accounts located in Argentina. And I remember us having to comply because we were regulated entity, and seeing the price of Bitcoin rise the same day. And it was really clear that a lot of Argentines at the time were actually moving their funds into Bitcoin so that they would have control over their hard-earned money.”

David Marcus, The Block, June 27, 2023

According to reporting from Financial Times, Marcus, a close confidant of Zuckerberg, apparently “texted Zuckerberg to outline his ruminations” and after successfully convincing Facebook’s CEO, he was given a “blessing to explore the idea further.” Marcus quickly outlined his idea in an internal memo, highlighting that “Facebook’s more than two-billion-strong user base” empowered with crypto “could offer a convenient and cheap way to move money around the world,” in addition to providing “a treasure trove of data about what people spend their money on.”

For the social network, the “possible multi-billion-dollar commercial opportunities were clear,” including “user transaction data,” “more engagement,” “more e-commerce,” and “a slice of fees from transactions.” According to an unnamed regulatory official, this “was always their advantage.” Libra would “create tremendous opportunity and a lot of money for them. But if Facebook was going to be the reason it was very successful, they were also going to be the reason it would fail.”

During the months right after Libra’s announcement, Marcus updated his thoughts on Bitcoin, stating “For me, now, it’s clearer that Bitcoin serves a purpose of being digital gold, not a good medium of exchange.” It was this axiom that led Marcus to express that “this was the right time for us to start thinking about how we could address the very things that blockchain and cryptocurrency were meant to do” and that “we had real solutions to bring to the fore.” Marcus later explained his motivations for bringing publicly-issued money via tokenized dollars to the Libra experiment in an August 2023 conversation with Bankless:

“I don’t think that I’m in the camp of people who want to fully separate money from State. I feel like my own personal objective is to actually make the underlying rails really efficient, really open, really interoperable, and enable more people to have access to them. I think that the world where actually good governments cannot control their own monetary policy, etc., this world where it doesn’t exist, would be chaos.”

It is perhaps this affinity for State-controlled monetary policy that led Marcus to announce Libra to the world within the confines of The Old San Francisco Mint in June 2019. However, the project itself was started both in earnest and in secrecy by Facebook in early 2018, when Morgan Beller, a former partner of Andreessen Horowitz, joined Marcus in plotting to bring both payments and a novel currency construction to Facebook’s Messenger product. According to reporting from the Financial Times, the pair first worked “in a small, empty room” with “walls adorned with whiteboards” within “Facebook’s main campus in Menlo Park.” Shortly after, the duo “moved to a larger, more secluded building” positioned “on the outskirts of the company’s headquarters” that limited access to “only employees with particular passes” consisting of “the crypto experts, engineers and economists.” The project was codenamed Libra, and Beller was quoted as saying that the team was “paranoid about leaks” and operated “like a secret Swat operation.”